We are excited to announce that we have joined forces with Intraprise. As a new combined organization, we have the opportunity to transform the current Level1Analytics product to the most capable and scalable valuation platform available on the market.

by Dr. Thomas J. Healy, CMB

Mortgage Defections: How to Measure and Maximize Your Recapture Rate

Thursday, September 11, 2025

What is your mortgage recapture rate? Most servicers don’t know.

Servicing is a self-liquidating asset. Over a thirty-year period, a typical mortgage loan amortizes down to zero. Since service fees are typically tied to the outstanding principal balance, service fee revenue also declines to zero. This liquidation of the servicing asset, while inexorable, is usually slow. A typical mortgage loses only 6% of its balance in the first five years. However, this issue is exacerbated by pay-offs. At a 10% CPR (conditional prepay rate), a mortgage portfolio loses 45% of its balance in the first five years of its life, and a comparable amount of value.

Assuming these are primarily refinancings, it should be close to a zero-sum game. In fact, if you had 100% market share, it would be a zero-sum game (absent the cost to refinance). Every loan that paid off would be immediately recaptured. The reality that this is not the case implies your customers are defecting to a competitor, not extinguishing their mortgages. Since servicing costs do not decline in tandem with service fees (they are typically a function of loan count, not principal balance), servicers that do not replenish run-off ultimately face the decision to either grow or exit the business.

The low-hanging fruit to minimize self-liquidation is, therefore, a marketing problem—not a financial one. It requires three steps:

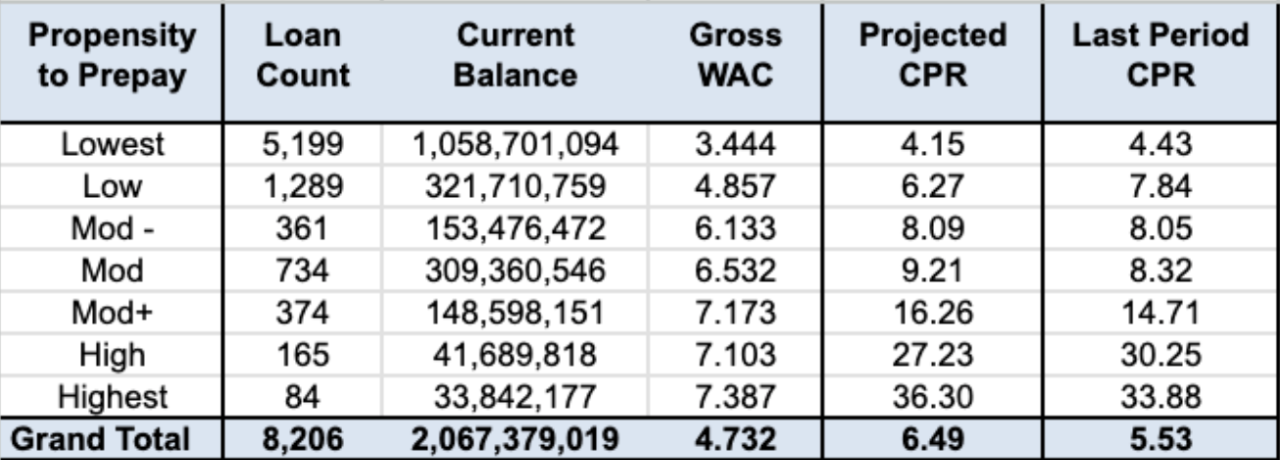

1. Identify existing loans with a high propensity to prepay (“PtP”). The Level1Analytics proprietary prepay model can help you identify these. This should be augmented by information from your customer service area highlighting mortgages that have requested pay-off balance or other similar inquiries.

2. Reach out to high PtP risk customers. Remind them you exist, offer mortgages, or even HELOCs. Given the lack of branding in our industry, many borrowers will not think of you first when refinancing. Instead, they may go with a broker recommended by a friend or relative.

3. Develop and maintain a Mortgage Recapture Rate metric to track retained customers by comparing the property addresses of paid-off loans with the addresses of new loans added. The goal should be to manage this metric as close to 100% as possible. Level1Analytics can assist in developing and monitoring this metric as well.

What is your mortgage recapture rate? As Peter Drucker said: “If you can’t measure it, you can’t manage it.” Why guess when you can know?

Stay Ahead of the Market: At Level1Analytics®, we track these dynamics in real-time to help institutions make smarter MSR and whole-loan portfolio decisions. Want to know what this means for your book?

Contact Us

Our team is hands-on and knowledgeable, reach out to us for any consultation needs or questions.

Email Us

info@level1analytics.com

Call Us

+1 954-483-3424